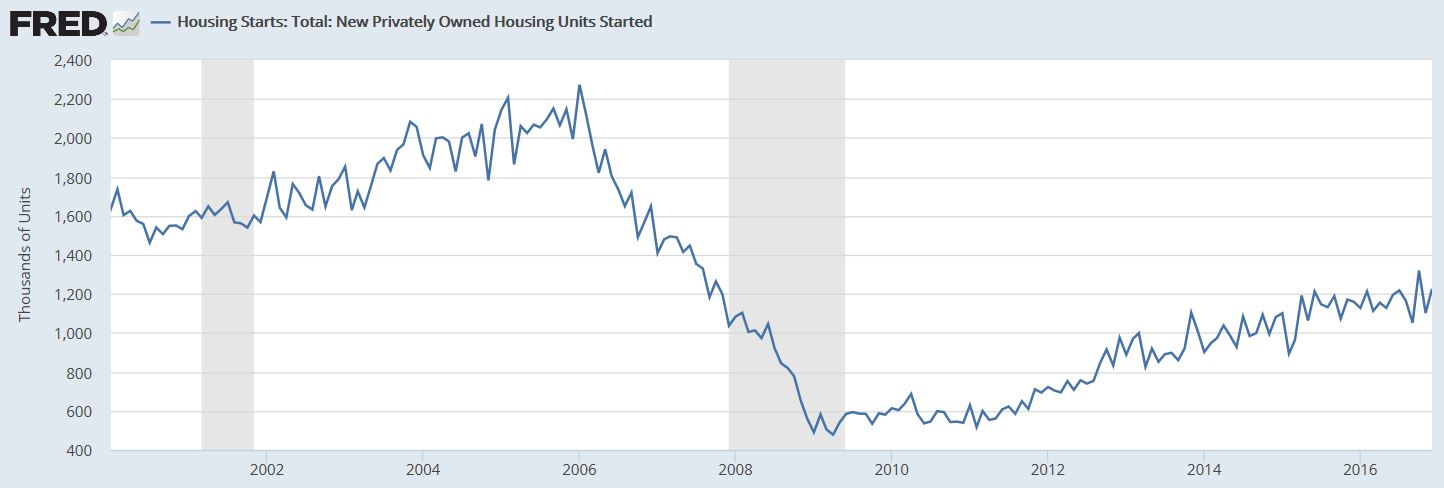

Following a drop in activity in November, US housing starts increased sharply in December helping the index to hit its highest level in nine years. An estimated 1.17 million housing units were started in 2016—a nearly 5 percent increase over 2015—making it the strongest year since 2007. However, there was a continued divergence in the types of residential buildings under construction; single-family starts were up 9.3 percent last year, but multifamily units fell 3.1 percent. A similar pattern was seen in permits data.

Housing Starts, Permits & Completions

Housing starts rose 11.3 percent to a seasonally adjusted annual rate (SAAR) of 1.23 million units in December. Single-family starts accounted for 795,000 units, which is 4 percent below the revised November figure of 828,000. The volatile multifamily segment rebounded 53.9 percent from a month earlier.

Building permits, an indication of planned construction, were down 0.2 percent to 1.21 million, although single-family permits increased 4.7 percent.

Regional performance was largely positive in December, as confirmed by the US Census Bureau report. Seasonally-adjusted housing starts by region included:

- Northeast: +18.5 percent; (-52.1 percent last month)

- South: -1.4; (-9.3 percent last month)

- Midwest: +31.2 percent; (-14.2 percent last month)

- West: +23.5 percent; (-22.1 percent last month)

While the yearly numbers are, generally speaking, good news for the economy, the historical context is lackluster when accounting for population growth. The number of single-family and multifamily starts per 1,000 households remains about 38 percent below the 50-year average according to Ralph McLaughlin, chief economist at Trulia, an online marketplace serving the real estate industry.

“When you look at single-family [construction] we’re still at recession levels, which is quite remarkable because historically the real-estate cycle leads the business cycle,” said Sam Khater, deputy chief economist at CoreLogic, a housing data firm.

Source: Federal Reserve of St. Louis (FRED), US Census Bureau

Economists are optimistic that single-family housing starts will continue to improve in 2017, as rising wages help drive demand. Republicans have pledged to ease environmental regulations and President Donald Trump has promised tax cuts and infrastructure spending that could help extend the economic recovery. “I am cautiously optimistic that 2017 is going to be an even better year and I hope it is for the sake home buyers,” McLaughlin added.

Mortgage Rates

The 30-year fixed mortgage rate jumped in December from 3.77 to 4.20. This is the highest monthly rate since April, 2014, and it represents an 11 percent increase over November’s rate, which is significant given the very shallow monthly changes we have seen for the better part of two years.

There is a lot of positive economic anticipation at present, as world markets react to a general sense of an improved business environment in the US. The larger housing market will continue to play an important role in keeping the economic engine running, but fresh research from the National Association of Home Builders (NAHB) illustrates a shift in homeownership trends that will likely impact the dynamic and impact of the housing sector.

Homeowner Trends & Outlook

Per the NAHB, the average size of newly-built homes decreased in 2016, a sign that the residential construction industry is preparing for the coming wave of first-time buyers as Millennials begin to (slowly) transition into homeownership. In 2015, the typical new home was 2,689 square feet; in 2016, it dropped to 2,634 according to figures from the US Census Bureau, which represents the first drop in size since 2009.

Per Rose Quint, NAHB assistant vice president for survey research, "The data on new home characteristics show a pattern. 2016 marked the end of an era that began in 2009 when homes got bigger and bigger with more amenities. I expect the size of homes to continue to decline as demand increases from first-time buyers."

First-time buyers are choosing amenities but in a package with an overall smaller footprint, which is not surprising given Millennials’ penchant for conservation and environmental awareness. Although, “necessary” new-home comforts include a separate laundry room, energy-efficient features (such as low-E windows), Energy Star-rated appliances, ceiling fans and programmable thermostats. These buyers also want their homes to have a patio, exterior lighting and a full bath on the main level. Regardless of income, buyers overwhelmingly prefer a smaller house with more features over sheer size. "More than two-thirds are willing to trade size for high quality products and features," Quint said.

But the financial situation of so many Millennials is making this transition considerably more difficult to achieve than it was for their parents. A recent report from national outreach organization Young Invincibles, The Financial Health of Young America: Measuring Generational Declines Between Baby Boomers & Millennials, sheds light on this discrepancy. The report analyzes the economic challenges facing today’s young people and looks at the financial security of Millennials compared to their parents. The findings are based on a cross-generational analysis of Millennials today compared to Baby Boomers when they were young adults.

Per the report, Millennials earns lower incomes, are less likely to own a home, and have lower net wealth than their parents’ generation at the same stage in life. Key findings include:

- Millennials have amassed a net wealth half that of Boomers at the same age.

- Young adult workers today earn $10,000 less than young adults in 1989, a decline of 20 percent.

- When baby boomers were young adults, they owned twice the amount of assets as young adults.

“These findings uncover that Millennials have been set back significantly, by not just the Great Recession but by decades-long financial trends, resulting in major generational declines in financial security between Millennials and Baby Boomers when they were the same age,” said Tom Allison, Deputy Director of Policy and Research for Young Invincibles. “Millennials make up the greatest share of the workforce and the largest generation in history, so in many ways the situation facing young adults today forecasts the financial challenges ahead for the nation.”

The report also outlines a bipartisan policy plan to help Millennials start building wealth, which includes the Earned Income Tax Credit, portable retirement plans, incentivizing ways to save tax refunds and more. “As the new administration and Congress take office this month, we urge them to consider these findings. We need policies that will help Millennials build wealth and make sure our generation doesn’t fall further behind,” said Allison.

The financial situation of millions of Millennials and potential home buyers is going to be a challenge for home builders in the near and long terms. Trulia’s McLaughlin added, “While some of the challenges that homebuilders face are cyclical, stemming from an historically abhorrent fiscal recovery that started with the Great Recession, many of the challenges are also structural. Decades in the making, the latter originated from the sea change of strict land regulations that swept much of the country during the 1970s and ‘80s. So while there is much room for growth in starts as the economy continues to grow, the recovery in new construction will be slow and steady because of these structural challenges.”