Suz-Anne Kinney

Suz-Anne Kinney

This post is excerpted from Forest2Market's monthly Economic Outlook, a 24-month forecast of macroeconomic indicators.

Industrial Production

After edging up by 0.1% in October (revised from -0.1%), the seasonally adjusted industrial production (IP) index gained another 1.1% in November. The bulk of November’s gain is attributable to utility output, thanks to colder temperatures. Performance of major sub-groups was as follows:

- Manufacturing advanced by 0.6%, besting October’s +0.5%. Manufacturing remained 3.6% below its pre-recessionary peak, however.

- Wood Products gained 3.1%, handily beating October’s 0.8% increase.

- Paper rose by 0.2%, slowing from October’s 0.8% increase.

- Construction was unchanged at 0.6%.

- Consumer Goods jumped by 1.5%, reversing October’s 0.1% decline.

Capacity utilization of all industries increased 0.8% in November (to 79.0%); both Wood Products (3.1%) and Paper (0.3%) expanded. Capacity among all industries nudged 0.2% higher in November; once again, Wood Products was unchanged while Paper shrank by 0.1%.

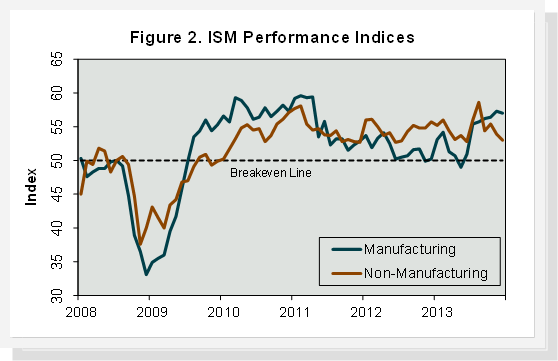

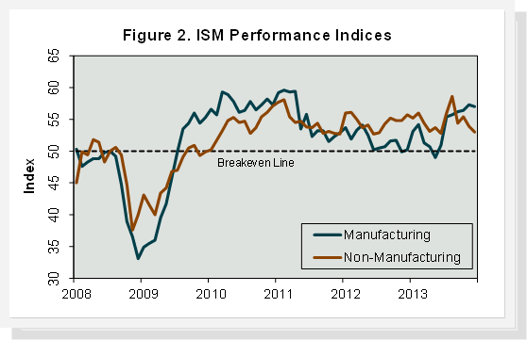

Manufacturing and Non-manufacturing

According to the Institute for Supply Management (ISM), expansion of economic activity in the U.S. manufacturing sector slowed slightly in December (Figure 2). The PMI registered 57.0 percent, a decrease of 0.3 percent from November's reading (50 percent is the breakpoint between contraction and expansion). “Comments from the [respondent] panel generally reflect a solid final month of the year,” said Bradley Holcomb, chair of ISM’s Manufacturing Business Survey Committee, “capping off the 2H2013, which was characterized by continuous growth and momentum in manufacturing.”

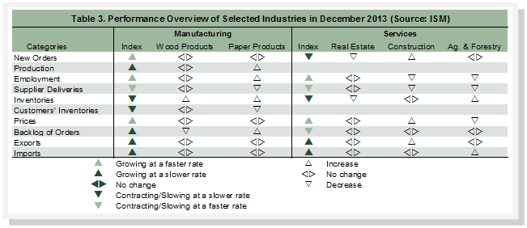

December’s general manufacturing sub-indices were mixed (Table 3): New orders, employment, deliveries and input prices all expanded relative to November. Production, order backlogs, and exports -- while still expansionary -- slowed from the prior month’s pace. Most encouraging (if it translates into increased 4Q2013 consumption), inventories contracted; this suggests the huge 3Q2013 inventory run-up is perhaps being drawn down by increased demand.

Both Wood Products and Paper Products expanded in December. In the case of Wood Products, with no change in eight of the ten categories, rising inventories outweighed the drop in order backlogs and pushed the ISM reading for the sector into the expansion column. "Markets are sound,” wrote one Wood Products respondent. “We typically see a seasonal 4Q slowdown. However, this year … not so." Paper Products’ expansion was based on broader support, including production, employment, and order backlogs; "Orders and price continue to be strong," observed one Paper Products respondent.

Growth in the service sector, which accounts for roughly two-thirds of the U.S. economy, slowed in December as well. The NMI registered 53.0 percent, 0.9 percentage point lower than in November -- and the lowest point since June. Employment, the pace of supplier deliveries and inventories rose at a faster pace. All other sub-indices either expanded more slowly or contracted in November. The most notable development was the tumble in New Orders (down from 56.4 to 49.4) -- the first contraction in the New Orders index since July 2009. “Despite the substantial decrease in the New Orders Index.” said Anthony Nieves, chair of ISM’s Non-Manufacturing Business Survey Committee, “respondents’ comments predominately reflect that business conditions are stable.”

Among the individual service industries we track, only Construction expanded (thanks to new orders and new export orders). Real Estate retreated under falling new orders and inventories. Ag & Forestry was unchanged.

Commodities up in price included corrugated packaging and wood. Some respondents indicated paying more for gasoline and diesel, while others paid less.