Suz-Anne Kinney

Suz-Anne Kinney

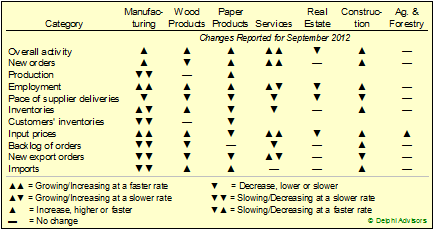

From Forest2Market's Economic Outlook:

Manufacturing moved back into expansion territory during September, with the PMI jumping up to 51.5 percent, from 49.6 in August. After reciting some report details, Bradley Holcomb, chair of ISM’s Manufacturing Business Survey Committee, concluded with, “Comments from the [respondent] panel generally reflect a mix of optimism over new orders beginning to pick up, and continued concern over soft global business conditions and an unsettled political environment.” The sub-indices were mixed: The number of respondents reporting increased new orders and employment rose, and new export orders contracted more slowly in the face of a dramatic rise in the number of respondents reporting higher input prices (see Table).

The service sector grew at a faster clip in September, reflected by a 1.4 percentage point rise (to 55.1 percent) in ISM’s non-manufacturing index (now known simply as the “NMI”). Comments by Anthony Nieves, chair of ISM’s Non-manufacturing Business Survey Committee, had the same tenor as Holcomb’s. “Respondents’ comments continue to be mixed,” said Nieves; “however, the majority indicate a slightly more positive perspective on current business conditions.” The mix of service sub-indices was somewhat more upbeat than was the case for manufacturing; the number of respondents reporting heightened business activity and new orders increased dramatically; however, the number of firms facing higher input prices once again rose noticeably.

Wood Products reportedgreater overall activity in September, including greater employment, increased imports, and increasing inventories. However, we would observe that expanding inventories coupled with falling new and backlogged orders may augur slowing activity for the sector in the near future. Paper Products’ expansion was more broadly based, with new orders, production, employment all up and inventories, customer inventories, and input prices all lower. The only clouds that might be on the horizon are from falling new export orders and higher imports and backlog orders holding steady.

Real Estate reported contraction in overall activity, thanks primarily to a drop in employment. Construction, by contrast, received broad-based encouraging news. One item of note for the wood producing sector relative to construction activity is that the import sub-index increased; with so much U.S. wood products capacity curtailed it seems odd imports would be needed to meet construction demand. However, construction imports include materials other than strictly wood-based materials and they may account for the increase.

The short-term outlook for American manufacturing jobs may be rather bleak, but the Boston Consulting Group (BCG) is very upbeat about longer-term prospects*. BCG recently predicted that manufacturing could repatriate between 2.5 and 5 million jobs by 2020. By as early as 2015, BCG predicts “the United States will have an export cost advantage of 5 to 25 percent over Germany, Italy, France, the U.K., and Japan in a range of industries [including machinery, chemicals, transportation equipment along with electrical and appliance equipment]. Among the biggest drivers of this advantage will be the costs of labor, natural gas, and electricity. As a result, the United States could capture 2 to 4 percent of exports from the four European countries and 3 to 7 percent from Japan by the end of the current decade. This would translate into as much as $90 billion in additional U.S. exports per year.” In addition:

- “America’s natural gas boom from shale (commonly referred to as ‘fracking’) has provided this country with some of the cheapest natural gas prices around the world. For the foreseeable future, natural gas prices will remain 50 to 70 percent cheaper in the United States versus Europe and Japan

- “Labor costs in other developed economies will be 20 to 45 percent more expensive compared with the costs of hiring U.S. workers

- “The United States could grab additional exports from the aforementioned nations to the tune of $130 billion annually

- “Average manufacturing costs in China will only be 7 percent lower compared to in the United States in 2015.”