4 min read

In areas of the West-South, significant rainfall, 400-800% higher than normal in some places, is contributing to flooding[i] and road closures.[ii] While it is too early for Forest2Market to analyze the effects of the West-South flooding on the timber industry, we think it likely that the effects will be similar to the impacts of the historic rainfall event in South Carolina in October 2015.

This analysis, Part 2 in a series of posts on the effect of significant rainfall on the forest products industry, describes the weekly impacts on roundwood (pine pulpwood, pine sawtimber and hardwood pulpwood[iii] procured from South Carolina counties in late 2015 by area of precipitation intensity, as shown in the following map. Part 1 of our analysis covered the impacts of a major precipitation event on wood supply and procurement patterns. This post looks at the impact of reduced supply on mill inventories and delivered prices.

Because Forest2Market collects detailed scale-ticket data that includes county of origin and destination facility for delivered wood, we are uniquely capable of quantifying the impacts of this storm and similar events on the industry. This analysis describes the weekly impacts on roundwood (pine pulpwood, pine sawtimber and hardwood pulpwood procured from South Carolina counties in late 2015 by area of precipitation intensity, as shown in the following map.

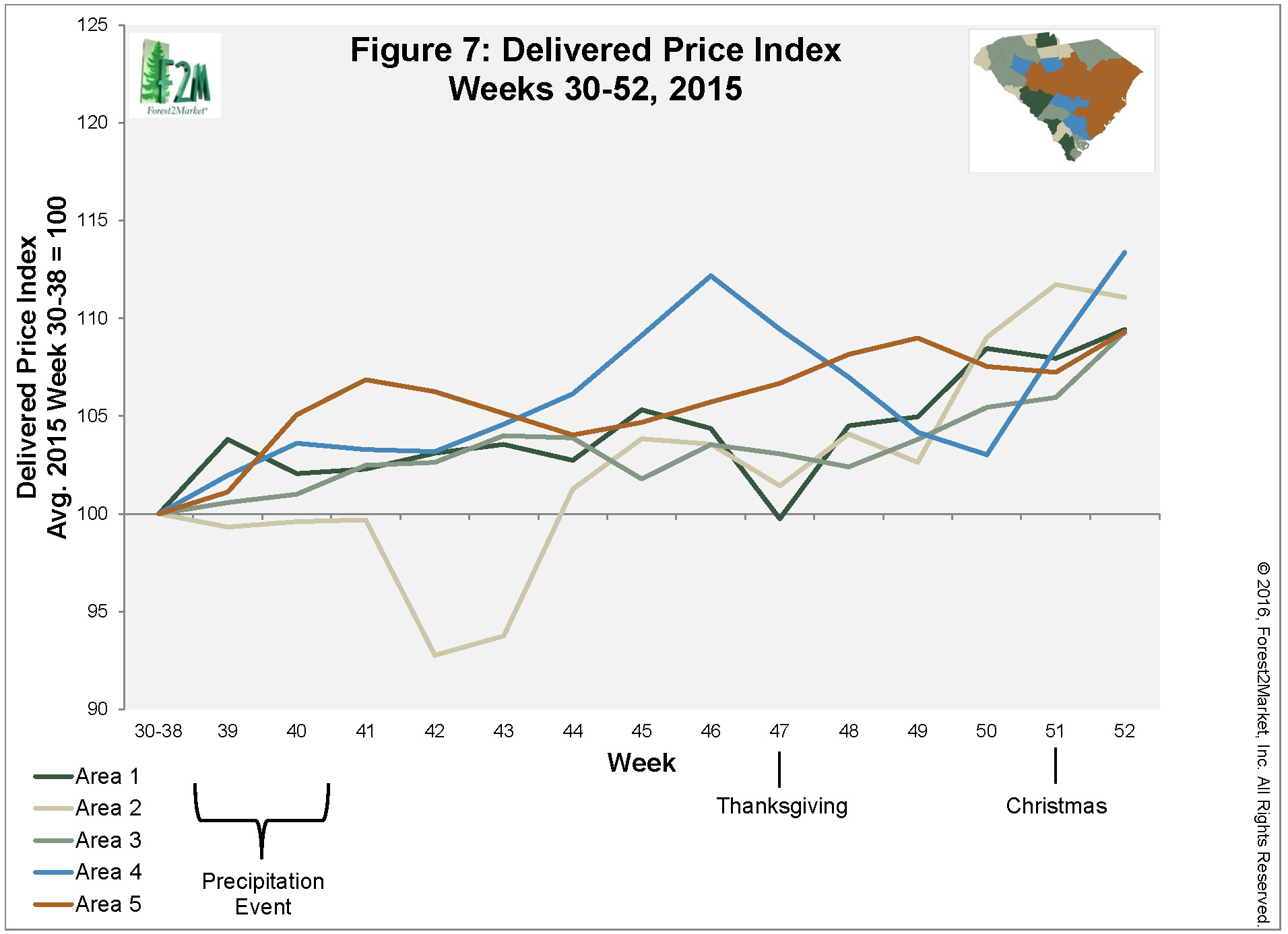

Primary precipitation fell during Weeks 39 (Sep. 27-Oct. 3) and 40 (Oct. 4-10) of 2015. Data are aggregated on a weekly basis based on the originating area for Week 30 through Week 52 of 2015 and 2014. Within each area, delivered prices for each year were indexed to the average delivered price during Weeks 30-38 of that year.

Impacts to Month-End Inventories and Delivered Roundwood Prices

The reduced supply available in 4Q2015 compared to 4Q2014 meant that mills had to either use their inventories, pay more for delivered wood, or both. A comparison of month-end inventories in South Carolina versus the rest of the U.S. South (Table 1) demonstrates that South Carolina mills were forced to rely on their inventories following the storm event. During the early part of the year, South Carolina mills averaged one additional day of inventory compared to mills elsewhere in the South. During each month of 4Q2015, however, South Carolina mills had 4 to 5 days less inventory than their counterparts in the rest of the South.

Figure 7 illustrates the impacts to delivered price that occurred in each area following the precipitation event. All areas except Area 2 experienced increases in delivered prices in Week 39 and 40.

The following charts show the changes in delivered price that occurred in late 2015 compared to the changes in delivered price that occurred in late 2014. For each year, delivered prices were indexed to the average delivered price for Week 30-38 of that year. While Areas 5 and 4 showed the most significant and persistent increases in delivered prices following the storm event, by Week 45 (Nov. 8-14), the delivered price in every area of South Carolina increased above the Week 30-38 average at a greater rate in 2015 than it did in 2014. While reduced supply was primarily a factor in Areas 5 and 4, increased demand in the other areas also led to price increases for delivered roundwood.

In Area 5, indexed delivered prices for late 2015 were higher than 2014 during each week, except Week 39 (Figure 8). The magnitude of the increase above Week 30-38 (Index=100) was much greater in 2015 than in 2014 due to the reduction in tons available on a weekly basis during much of this time period.

The story in Area 4 is very similar to that of Area 5 (Figure 9). In late 2014, delivered prices were lower in Weeks 39-52 than they were in Weeks 30-38. In 2015, delivered prices were consistently higher than they were in Weeks 30-38.

In Area 3, both 2014 and 2015 delivered prices increased after Week 39 of the year (Figure 10). For all weeks except Week 39 and the holiday weeks, delivered prices increased above the Week 30-38 average at a higher rate in 2015 than they did in 2014.

In Area 2, 2014 delivered prices increased above the Week 30-38 average price during Weeks 39-46 and again in Weeks 48-52 (Figure 11). In 2015, however, delivered prices fell below the Week 30-38 average during Weeks 39-43. By Week 45, weekly indexed delivered prices for 2015 had increased above the increases observed in 2014.

In 2014 in Area 1, delivered prices increased briefly in Weeks 39-40 before staying fairly close to their Week 30-38 average until the end of the year (Figure 12). The pattern for 2015 is fairly similar. However, indexed 2015 delivered prices trended higher than 2014 prices in all weeks except Week 39, 40 and 47.

Implications for the Forest Products Industry

2015’s record precipitation and flooding event in South Carolina provided a unique opportunity to demonstrate the impacts of significant, widespread precipitation events on the forest products industry and its supply chain.

There were several notable findings from Part 1:

- Areas hit hardest by rain will experience both short (1-2 weeks) and possibly also long-term (in this case, 12+ weeks) decreases in supply.

- Supply shortages will lead suppliers to shift harvest activity to areas with less storm impact.

Part 2 of this analysis found the following:

- Precipitation events that interfere with the ability of suppliers to get wood to the mill cause mills to deplete their available inventories more heavily than planned.

- Supply disturbances result in immediate increases in delivered prices as mills compete for a reduced supply of wood and suppliers struggle to deliver wood to area mills.

- Delivered price impacts occur for wood both from the hardest hit areas, which have reduced supply, and neighboring areas, which experience an influx of demand.

The impacts of precipitation events on haul distances and supplier margin will be covered in Part 3, the final part of this series.

[i] https://weather.com/storms/severe/news/historic-south-flooding-march-2016. Retrieved 03/16/2016.

[ii] http://wwwapps.dotd.la.gov/administration/announcements/home.aspx?type=roadandlaneclosure. Retrieved 03/16/2016.

[iii] Forest2Market does not collect delivered hardwood sawtimber data in the U.S. South.