4 min read

This post is Part 3 of a series on the impacts of major precipitation events on the forest product industry using the historic rainfall event in South Carolina in October 2015 as a case study. Part 1 covered the impacts of major precipitation events on wood supply and procurement patterns while Part 2 analyzed the impact of reduced supply on mill inventories and delivered prices. This final installment analyzes the relationship between haul distances and supplier margins during and following major precipitation events.

Because Forest2Market collects detailed scale-ticket data that includes county of origin and destination facility for delivered wood, we are uniquely capable of quantifying the impacts of this storm and similar events on the industry. This analysis describes the weekly impacts on roundwood (pine pulpwood, pine sawtimber and hardwood pulpwood[i]) procured from South Carolina counties in late 2015 by area of precipitation intensity, as shown in Figure 3.

Primary precipitation fell during Weeks 39 (Sep. 27-Oct. 3) and 40 (Oct. 4-10) of 2015. Data are aggregated on a weekly basis based on the originating area for Week 30 through Week 52 of 2015 and 2014. Within each area, we report the weekly percentage change in haul distance and stumpage+supplier margin during Weeks 30-52.

Weekly Changes to Stumpage Price + Supplier Margin and Haul Distances

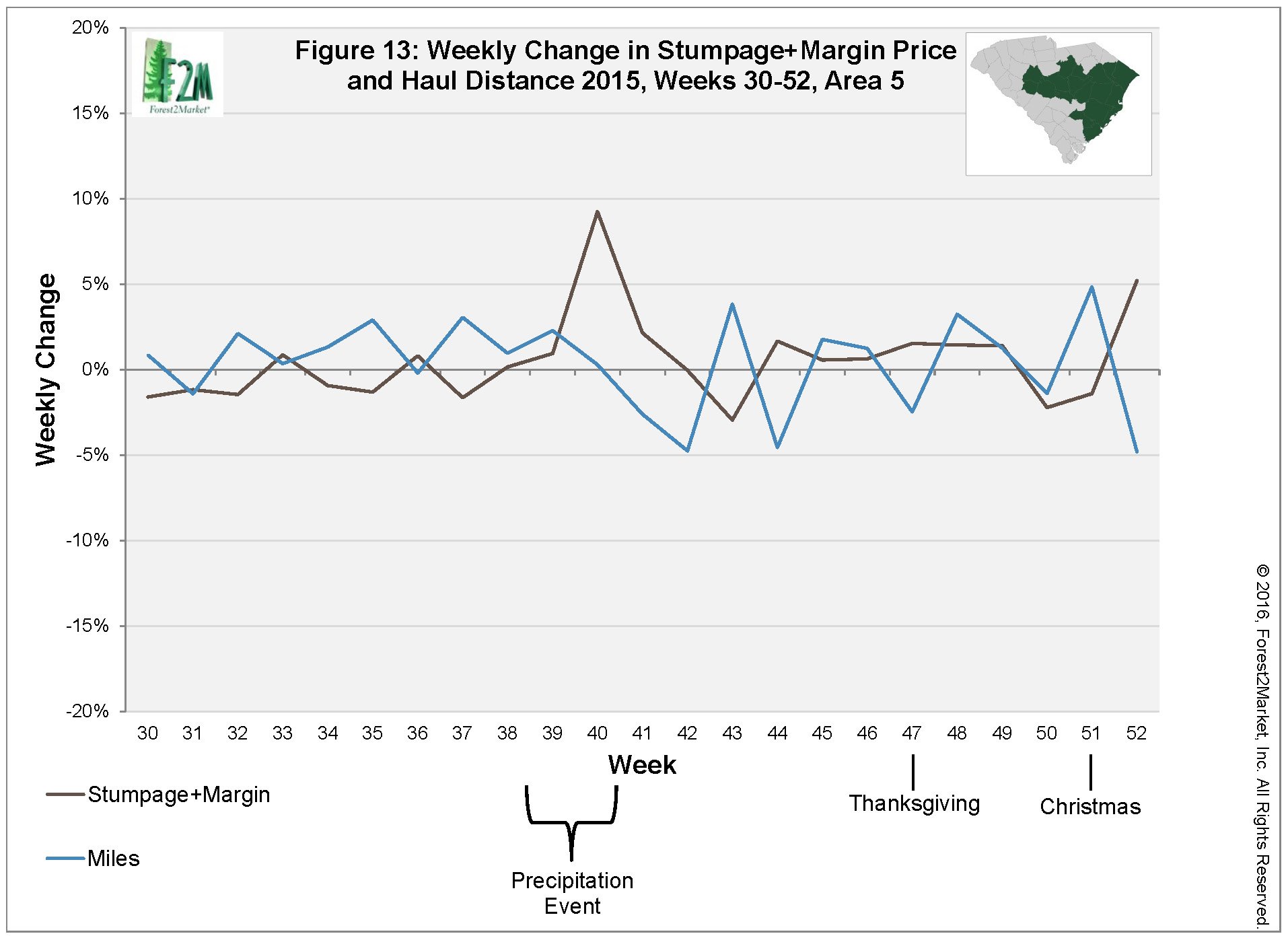

Prior to the storm event, stumpage prices (including supplier’s margin) in Area 5 experienced very little week-over-week fluctuation, changing less than 2% weekly as supply generally kept pace with demand (Figure 13). Reduced supply in this area during the storm, particularly in Week 40, resulted in a 9% increase to stumpage+margin while haul distances increased approximately 2% over the previous week. Weekly stumpage+margin prices continued to increase through Week 41. Stumpage+margin took a hit in Week 43 as haul distances to the mill gate increased. Throughout the period shown, the inverse relationship between stumpage+margin and haul distance is readily apparent: Increased haul distances chip away at suppliers’ margins and the price paid to landowners.

In Area 3, miles declined in both Week 39 and 40 while stumpage+margin prices increased less than 1% (Figure 14). Stumpage+margin increased by 2% or less each week during Week 39-44 before experiencing greater volatility leading into the holiday period. Area 3 absorbed the added demand from Areas 4 and 5 with a slow and consistent increase in prices in the weeks following the storm.

In Area 4, stumpage+margin prices had been on a declining or flat trend during Weeks 30-37 (Figure 15). Weekly stumpage prices increased fairly significantly in Week 38 before the storm hit. In Week 39, haul distances for wood purchased from this area increased 5% and stumpage+margin increased 1% from the previous week. Stumpage+margin increased an average of 3% weekly between Week 39 and Week 46.

Area 2 experienced sizable (8-12%) weekly increases to stumpage and margin price in Week 39, 44, 48 and 50 (Figure 16). Haul distances decreased substantially in Week 39 and Week 42 from previous weeks.

Much like Area 2, Area 1 experienced much greater volatility in stumpage+margin price and haul distance (Figure 17). In Week 39, stumpage+margin increased 4% from the previous week while miles decreased 9%. In Week 40, stumpage+margin decreased 8% while miles increased 14%. Notable weekly increases in stumpage+margin occurred in Weeks 42, 45, 48 and 50.

Implications for the Forest Products Industry

2015’s record precipitation and flooding event in South Carolina provided a unique opportunity to demonstrate the impacts of significant, widespread precipitation events on the forest products industry and its supply chain.

There were several notable findings from Part 1:

- Areas hit hardest by rain will experience both short (1-2 weeks) and possibly also long-term (in this case, 12+ weeks) decreases in supply.

- Supply shortages will lead suppliers to shift harvest activities to areas with less storm impact.

Part 2 of this analysis found the following:

- Precipitation events that interfere with the ability of suppliers to get wood to the mill cause mills to deplete their available inventories more heavily than planned.

- Supply disturbances result in immediate increases in delivered prices as mills compete for a reduced supply of wood and suppliers struggle to deliver wood to area mills.

- Delivered price impacts occur for wood both from the hardest hit areas, which have reduced supply, and neighboring areas, which experience an influx of demand.

In Part 3, we learned:

- Shifting harvest patterns to higher, dryer areas results in increased haul distances to the mill and reduced supplier margins.

As this analysis demonstrates, the wood supply chain is much like a living organism -- expanding, shifting and contracting as supply and demand interact and change. When faced with a supply deficit caused by a weather event, wood suppliers must continue to earn a living and mills must continue to operate. Mills will turn to their inventory in the short-term while wood suppliers will seek out higher, dryer ground that may be farther from consuming mills. As competition for accessible resources increases, delivered prices increase at rates that are higher than they typically are. These increases are driven primarily by increases in stumpage prices and supplier margin due to a tighter supply, but higher freight costs associated with shipping wood over longer distances also play a role. In general, suppliers who must haul over longer distances will also sacrifice margin in order to deliver product, and, as such, there is typically an inverse relationship in the weekly change of margin and haul distance.

Maintaining a resilient supply chain is of critical importance. Suppliers’ ability (or inability) to adapt to changes in available supply will determine how well (or how badly[ii]) the precipitation event impacts their operations. Likewise, the ability of mills to “weather the storm” will rely on their level of preparation for such events (i.e. wood inventory and other contingency plans) and the strength and resiliency of their suppliers.

By using transaction data to analyze mill or supplier performance during supply disruptions, forest products companies - whether they consume pine or hardwood, sawtimber or pulpwood, primary or secondary chips -can identify strategies to help them deal with future disruptions more efficiently.

[i] Forest2Market does not collect delivered hardwood sawtimber data in the U.S. South.

[ii] http://www.blufftontoday.com/bluffton-news/2015-12-07/south-carolina-loggers-mills-struggling-after-flood#.VthrL-b-sXc