Daniel Stuber

Daniel Stuber

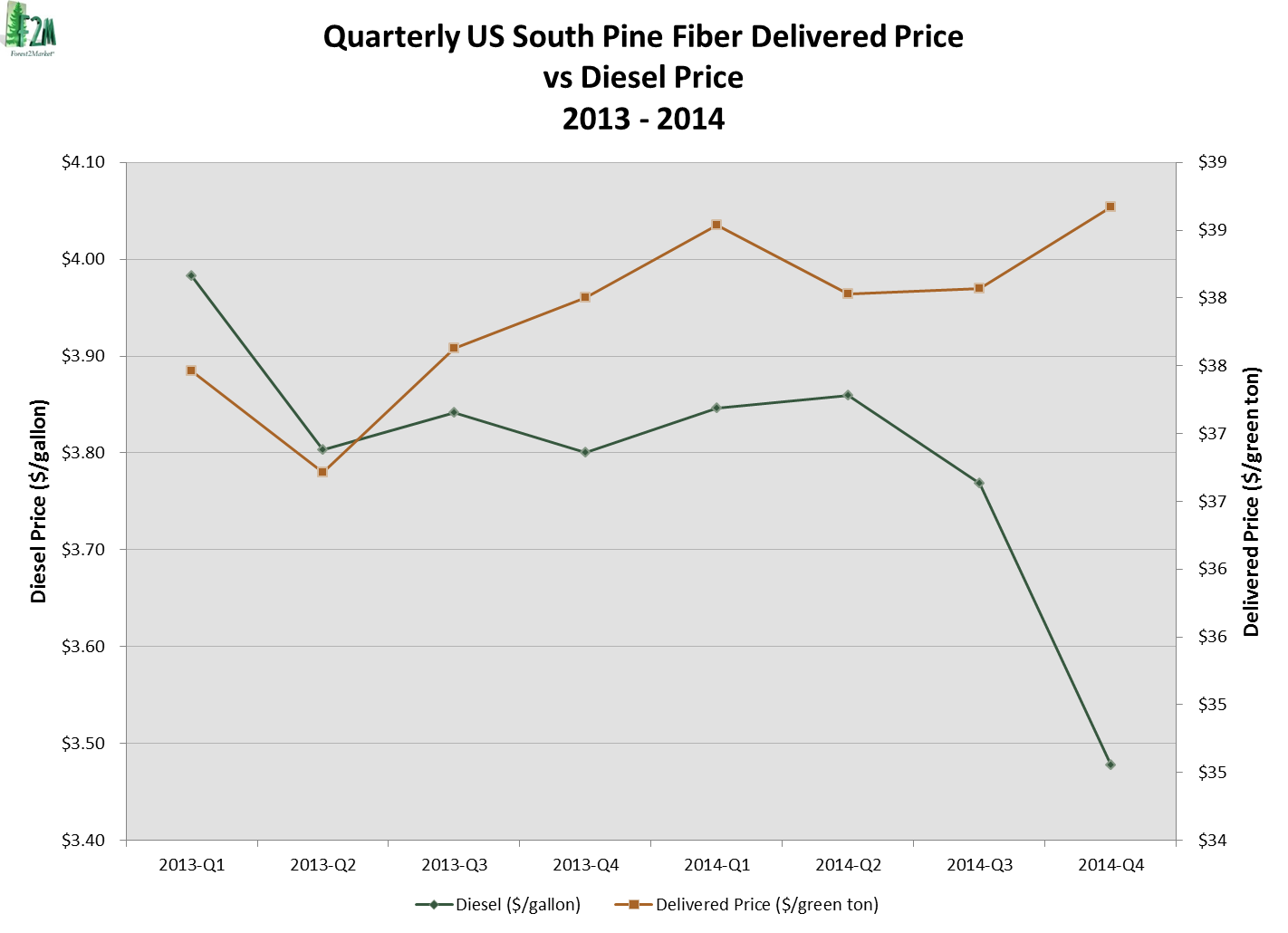

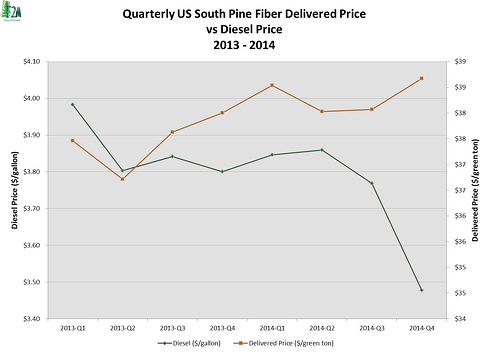

Recently, one of our pulp and paper customers asked us to help him explain to his CEO why his company’s delivered wood fiber prices were not declining as the prices of oil and diesel were falling (Figure 1).

His explanation—one we both thought was right—was that other factors, including weather, demand and inflation exerted more influence on delivered fiber prices than diesel. Since applying data to answer questions and solve problems is in Forest2Market’s wheelhouse, we analyzed the delivered price data from the Forest2Mill® benchmark service to substantiate his explanation. With a limited time and scope, we put together the following correlated metrics for his presentation to the CEO.

Note: For those out there unfamiliar with the term, correlation coefficient is a statistical measure used to determine the strength of a relationship between data; the closer this number is to 1.0, the stronger the relationship between the variables.

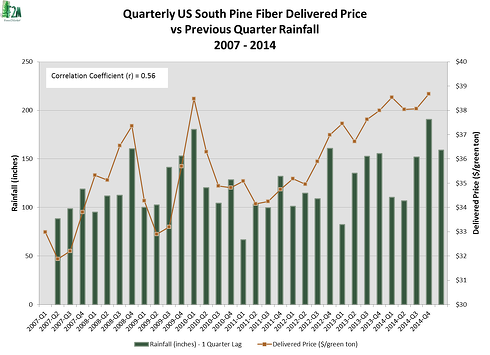

Weather: The Usual Suspect

Ask any forester about what influences delivered fiber price, and 9 out of 10 will answer “weather”. As a company of foresters, naturally, we chose weather as our first metric. Using data from the National Oceanic and Atmospheric Administration, we correlated quarterly precipitation data in the US South to pine fiber (both pulpwood and chips) delivered prices (Figure 2). The data was positively correlated and the relationship became stronger when lagged by a quarter (correlation coefficient (r) = 0.56); that is, wet weather causing tightened supply in one quarter will cause prices to rise in the following quarter. The trend chart told a more complex story, however. The lag appeared to exist until 1Q2012. At this point, the trend disappeared and no lag could be identified. While we did not test this assumption, it appears to show the lag was stronger on a monthly—not quarterly—basis.

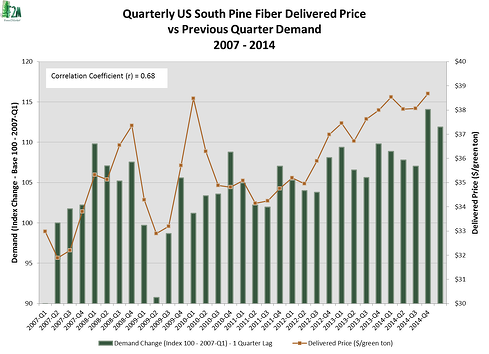

Demand: More, More, More

After examining weather, the next logical suspect was that increased demand could be pushing prices higher. Using the scaled purchase tons from Forest2Mill® and indexing the percent change from quarter-to-quarter (1Q2007 = 100), we correlated demand to delivered price (Figure 3). As with the weather correlation, the data was positively correlated and became stronger when lagged by a quarter. In addition, demand had a higher correlation coefficient (r = 0.68) than the correlation with precipitation. Read Pete Stewart's Wood Fiber Supply Chronicles, Part 1, for more information on demand.

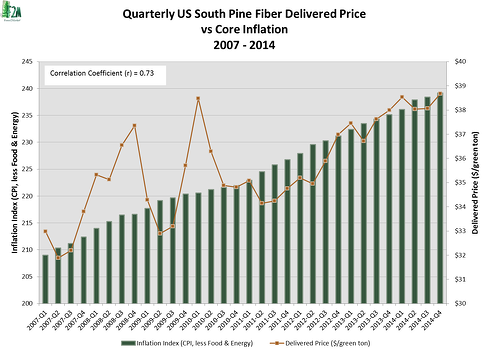

Inflation: What Goes Up

Our search for the answer next turned to inflation. We examined core inflation using the Consumer Price Index (CPI), Urban Consumers: All Items, less Food & Energy. On a trend-line basis, the data was positively correlated with a correlation coefficient of (r) = 0.73 (Figure 4).

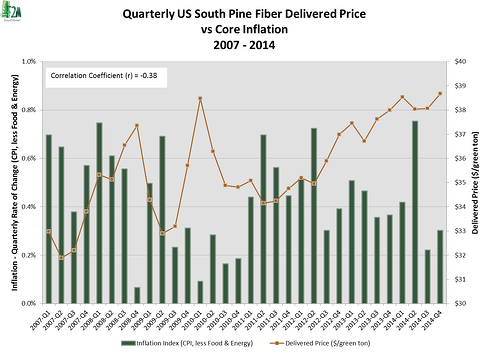

However, this denotes that delivered prices follow inflation over the long-term. On the short-term, we measured the quarter-to-quarter change in CPI, and found the data to be negatively correlated with a correlation coefficient (r) = -0.38 (Figure 5).

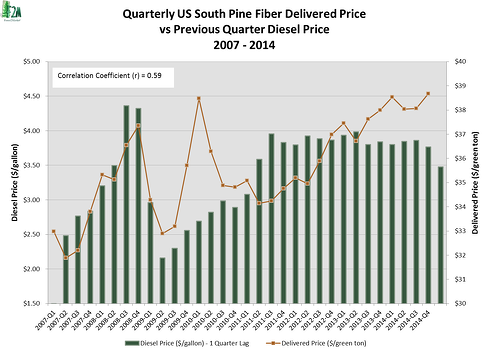

Diesel: Must Come Down

Finally, we decided it was time to test the variable at question: diesel price. We used the U.S. Energy Information Administration’s Ultra-Low Sulfur, On-Highway Diesel prices for the Lower Atlantic (PADD 1C) and Gulf Coast (PADD 3) regions. As expected, the diesel average was positively correlated with a correlation coefficient (r) = 0.59. Unexpectedly, the correlation was stronger than the correlation with precipitation; (r) = 0.59 vs 0.56.

Final Assessment

The correlation with diesel placed us in a quandary to help support our customer’s explanation. While not as strong as the correlations with demand and inflation, the decrease in diesel prices should have had some downward impact on price. Since the market is made up of a combination of factors, each exerting either upward or downward pressure on price, for our final assessment we decided to test all the variables together in a linear regression model to measure each for significance and determine if and how the variables may be related.

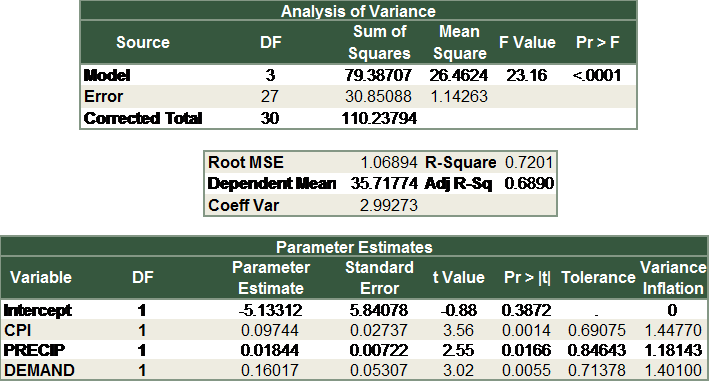

When each of the factors we tested—weather, demand, inflation and diesel were combined—the model rejected diesel as a driver of price. Of the remaining factors, in terms of significance, precipitation was less significant than inflation and demand (where P-values (Pr > |t|) less than 0.01 is preferred for a 99% confidence interval).

A multitude of variables contribute to delivered price other than just oil and diesel. Supply, demand and macro- and micro-economic variables are just some examples. Though simple, the above metrics demonstrate that diesel is not as significant to explaining delivered price as many may expect.

For those who would like the statistics, here are the final model results: